How CESECO Unlocks Untapped Animal-Waste Energy—and Creates a Margin Hedge for Every Refiner

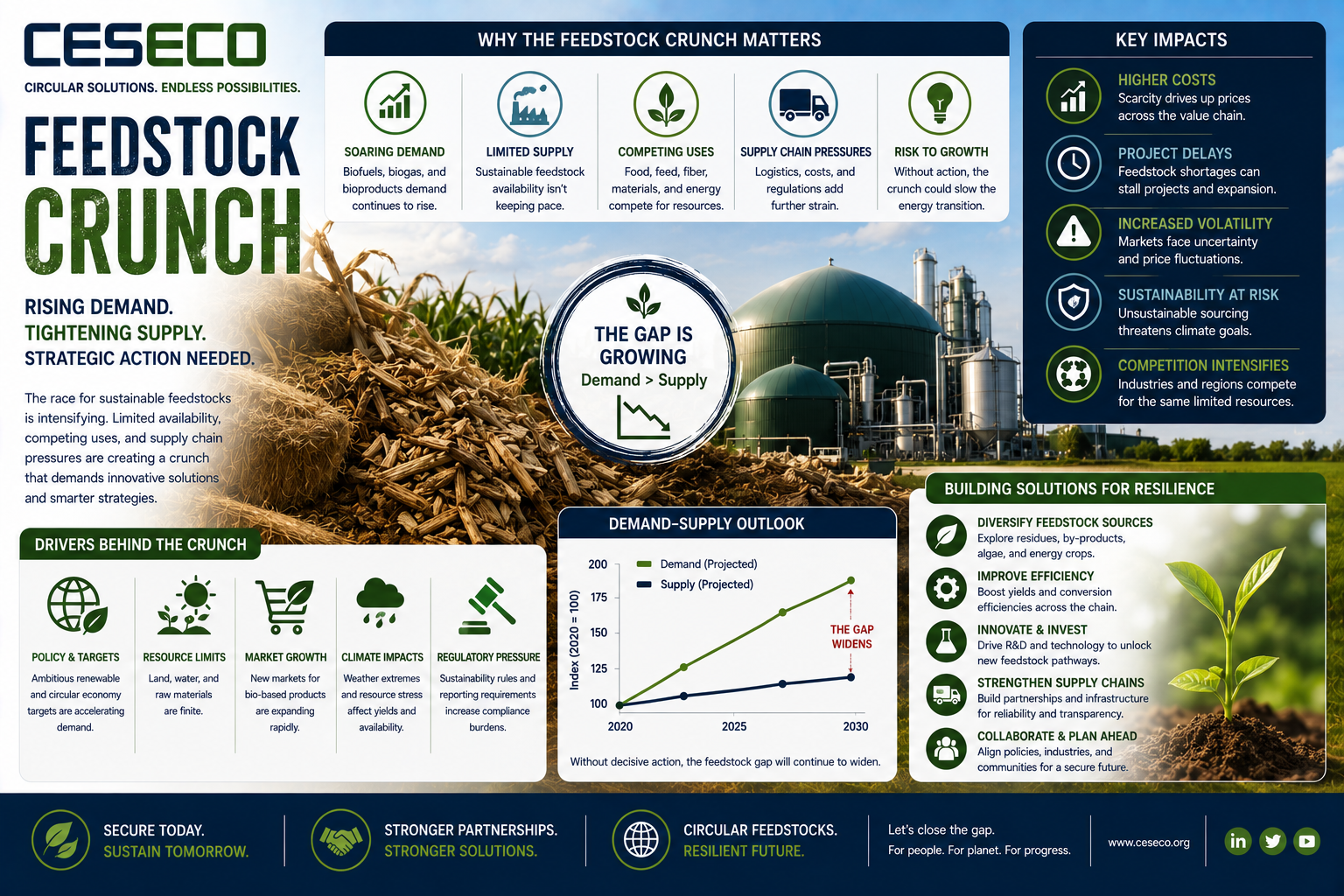

Global biofuel capacity is rocketing, but the barrels to feed it are not. The International Energy Agency warns that demand for vegetable oil, waste fats and residues will jump 56 % by 2027, led by renewable diesel and sustainable aviation fuel. fastmarkets.com Used-cooking-oil (UCO)—today’s work-horse lipid—already trades at record premia and is dominated by long-haul imports from China and the US. The question on every refiner’s mind: what happens when the taps run dry or prices spike?

The overlooked answer sits in the meat aisle

Each year Europe’s slaughterhouses generate millions of tonnes of Category 1 & 2 by-products that never reach the dinner plate. Most is incinerated or rendered into low-value tallow. CESECO upgrades this biomass into HEFA-grade bio-fats, nutrient-rich fertiliser and baseload green power—wringing profit from a stream others ignore. Our proprietary process recycles 100 % of incoming material and cuts lifecycle CO₂ by 95 %. ceseco.org

Why refiners need CES in the supply mix

- Diversification = resilience. Locking in animal-waste lipids alongside UCO hedges price and fraud risks (no one dilutes cow fat with palm oil).

- Domestic molecules, local ESG wins. UK-sourced feedstock slashes scope-3 shipping emissions and future-proofs RTFO compliance if import scrutiny tightens.

- Stable index-linked pricing. Gate-fee economics mean our feedstock costs track waste-management fees, not soybean futures—decoupling refinery margins from food-price shocks.

Why investors should lean in now

- Multi-revenue engine. Gate fees, bio-fat sales, green-power PPAs and fertiliser offtake create four income streams—each with inflation protection.

- Policy rocket boosters. England’s 2025 food-waste-separation law and the EU’s 2030 waste-reduction targets funnel extra feedstock to our gate; UK and EU SAF quotas pull product through the other end.

- Double-digit returns, real assets. One Eco Park processes 320 ktpa, throws off £40 m+ EBITDA and pencils a 12–14 % un-levered IRR without heroic price assumptions. That’s infrastructure-grade yield wrapped in an impact story.

The macro tailwind you can touch

- Demand up, supply flat. Adding 115 000 t of UK SAF each time the blend rises one point magnifies the feedstock gap.

- Import fragility. Regulators are already probing UCO origin fraud; future tariffs or bans could arrive overnight.

- Carbon math under scrutiny. Animal-waste lipids carry among the lowest CI scores in GREET and EU default values, giving refiners the best bang per tonne of CO₂ saved.

Near-term catalysts that lock in value

- Q4 2025 – Financial Close: first UK Eco Park fully funded; EPC contract executed.

- Q2 2026 – Feedstock MoUs: three EU protein majors commit 70 % of volume.

- Q3 2026 – Offtake Deals: two refiners sign 5-year purchase agreements for bio-fats indexed to RED certs.

- H1 2027 – Commissioning: first cargo delivered as IEA’s forecast crunch materialises.

Each milestone tightens our supply moat and raises the comp-set multiple.

What’s in it for the UK?

- Green jobs: ~150 direct positions per park plus 300 in logistics, engineering and farming.

- Energy security: local, circular feedstock that can’t be blockaded in a geopolitical spat.

- Export upside: surplus bio-fats qualify for US and EU credits, bringing hard currency home.

Secure your slice before capacity caps out

Refiners, blenders, investors: book your virtual tour or access our dataroom at ceseco.org, or DM me directly. Early partners lock in pricing, equity warrants, and bragging rights for solving the feedstock crunch before it bites.